The Fee Trap

Why Most GCs Are One Cycle Away From a Profitability Crisis

The construction industry grew revenue 7.9% last year. Strip out data centers and the picture collapses. Total construction spending fell 1.4% in 2025. Office spending excluding data centers dropped 17%. Warehouse fell 7.7%. Manufacturing, the darling of 2023 and 2024, is down 5% from its August 2024 peak and still falling. Private nonresidential activity is down nearly 7% from its January 2023 peak.

The industry is not growing. Infrastructure, AI and data centers as categories are growing, and everything else is contracting around it.

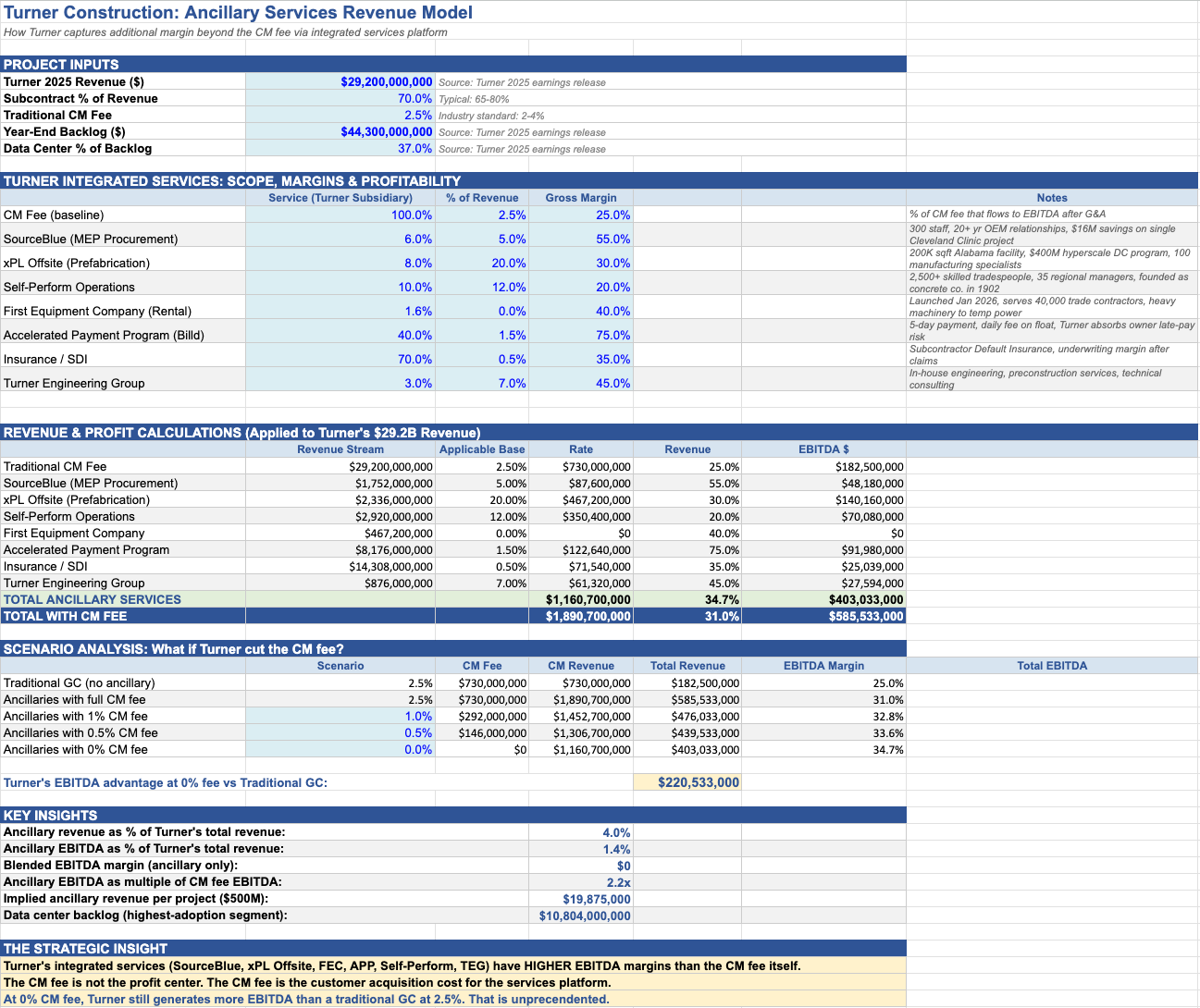

Turner is subtly showing everyone what happens when you stop treating the CM fee as the core business model. Turner did $29.2 billion in revenue in 2025, a 40% increase from 2024, with a $44.3 billion future backlog. Data centers represent 37% of that backlog. Turner is riding the same wave as everyone else through mission critical work but the difference is what Turner built as they’re riding the wave.

If you just want to see the model, skip to the bottom.

The data center mask

According to the Dodge Momentum Index, the industry grew 0.9% in April 2025. Without data centers, it would have dropped 3%. That’s a concerning drop in planning/momentum.

This is the construction industry’s version of the “magnificent seven” problem in equities. A small number of projects in a single asset class are carrying the entire market’s growth statistics. The ENR Top 400 reported $600 billion in total revenue for 2024, up 7.9%. Median firm revenue was flat with only 64.8% of firms reporting revenue growth, down from 77.3% the prior year. A quarter of firms said their backlogs shrank.

The firms posting outsized growth are the ones with data center exposure: Holder jumped from No. 30 to No. 15. HITT leapt from No. 26 to No. 10. Turner stayed at No. 1 and widened its lead. Barton Malow dropped from No. 19 to No. 35. The top of the ENR list is increasingly a ranking of who has the most hyperscaler relationships, not who is the best builder.

This concentration has a shelf life. Hyperscaler capex grew roughly 60% in 2025, and consensus expects that to decelerate to 20% in 2027, though Goldman Sachs has noted that consensus has underestimated actual spend by more than 30 percentage points in each of the last two years. The boom will continue to peak. But when it slows, the correction will land harder than the market expects, because the baseline expectation reset. A 20% deceleration off $660 billion is not the same as a 20% deceleration off $300 billion. The construction pipeline downstream of these commitments doesn't adjust at the same speed as a capex line item on an earnings call. Explicitly, the concerning part is that contractor backlog gets worked off faster than new projects enter the pipeline.

This is identical to what happened in manufacturing construction. Starts peaked in 2022 and 2023. Spending peaked in Summer 2023. Now manufacturing spending is declining ~5%% annually and the taper has just begun. The same pattern will eventually hit data centers. The only question is when.

The fee problem nobody wants to discuss

When the cycle turns, here is what every GC in the ENR Top 100 will face: the same amount of overhead spread across fewer projects, competing for work against firms that can afford to bid lower because their P&L does not depend on the CM fee.

A traditional GC on a $500 million project can earn a 2.5% CM fee ($12.5 million), converting maybe 25% to EBITDA ($3.1 million), and that’s the bulk of business. The fee is the margin. However, the margin is thin. And when backlogs shrink, fees compress as every GC with capacity is chasing the same shrinking pool of work.

The counterposition Turner just demonstrated is a wildly different model. In its 2025 earnings release, the company named six integrated services businesses:

SourceBlue (procurement, 300 people, 20+ years of OEM relationships)

xPL Offsite (prefabrication, 200,000 square foot factory in Alabama)

Self-Perform Operations (2,500 tradespeople, 35 regional offices)

First Equipment Company (equipment rental, launched January 2026, serving 40,000 trade contractors)

Turner Accelerated Payment Program (supply chain finance through Billd, Turner absorbs late-pay risk)

Turner Engineering Group

On the same $500 million project, these services would generate an estimated $23.5 million in ancillary revenue at a blended 38% EBITDA margin, producing roughly $9 million in EBITDA. That is ~2.6 times the EBITDA from the CM fee alone.

The implication that should keep GC executives awake: Turner has the option to bid 0% on the CM fee and still generate $5.8 million more EBITDA on the project than a traditional GC earns at just 2.5%.

Read that again. Zero percent fee. More profit.

This is a structural problem, not a cyclical one

In a rising market, fee compression is annoying but survivable. You lose a point on fee, but you make it up in volume, so the absolute dollar value increases. In a declining market, fee compression is existential, because you lose the point on fee and you lose the volume.

Turner’s ancillary services model inverts this dynamic. When the market contracts, Turner has two options that most GC’s can’t match. First, it can hold its CM fee steady and earn ancillary revenue on top, using the surplus to invest in capacity while competitors retrench. Second, it can cut the fee to zero, win every project it wants, and still maintain attractive margins on the ancillary services that flow through its platform.

This is the 1990s defense contractor consolidation playbook applied to construction. After the Cold War drawdown, the number of prime defense contractors fell from 51 to 5. If you were a company that already provided integration capabilities (systems engineering, logistics, maintenance contracts) and sold services around those capabilities, you were well positioned for the drawdown. That inversion of revenue generation from projects to services applies to construction.

By 2030, I’d expect the construction industry to have 50 large GCs where 5 will dominate and have optionality, and more importantly, agency of their future.

The AI capex dependency

The catalyst of change will be AI scaling laws affecting capex commitments from hyperscalers and foundational model companies.

AI-related business investment accounted for roughly half of inflation-adjusted GDP growth in the first half of 2025. Hyperscaler capex is projected at ~$600-660 billion for 2026. BCA Research’s chief global strategist has said that without the AI boom, the economy would plausibly already be in recession. Deutsche Bank notes that private business investment outside of AI-related categories is flat.

The construction industry’s exposure to this single variable is staggering. Data center construction hit a $45 billion annual rate in December 2025. Relatively small, but it is the only category with sustained growth and growing momentum. The pipeline of future work, outside of data centers and infrastructure, is contracting based on AIA starts and the Architecture Billings Index.

If AI scaling laws encounter diminishing returns, if hyperscaler revenue growth fails to justify the capex, if interest rates stay elevated or if debt-funded data center builds slow down, the construction industry loses its only growth engine. And firms that over-indexed on mission critical work that jumped 15 spots on the ENR list in a single year will face the sharpest reversals.

To be clear, Turner will face revenue pressure too. 37% of its backlog is data centers. But Turner’s ancillary services platform means its per-project profitability does not depend on the sector mix. Whether it is building a data center, a hospital, a stadium, or a pharmaceutical facility, the same SourceBlue procurement engine, the same xPL prefabrication capability, the same FEC equipment rental, the same Accelerated Payment Program all generate margin on top of whatever fee Turner negotiates.

So why isn’t anyone concerned?

Three reasons.

First, backlogs are still high. The ENR Top 400 is running on work sold in 2024 and 2025, when the market was stronger. It takes 18 to 24 months for a backlog decline to show up in revenue. The pain has not arrived yet, so it does not feel real.

Second, the industry does not think in terms of business model risk like the financial or insurance industries. Construction executives typically think about project risk, labor risk, material risk. The idea that your business model itself is a vulnerability, that the CM fee structure is a trap, is foreign to an industry that has operated the same way for decades. I’ve yet to see a BuiltWorlds or ENR Top 400 conference session about ancillary revenue diversification. They are talking about BIM, lean, AI, and safety culture.

Third, Turner is quiet about this, as they should be. Even the earnings release buries the integrated services narrative in a single paragraph. The strategy is visible only if you map the subsidiaries, model the economics, and compare the resulting P&L to a traditional GC’s. Turner has no incentive to advertise the fact that it can underprice every competitor and still make more money.

The omission is the signal though.

What this means for GCs

If you run a general contracting firm and your core margin comes from the CM fee, you have a defined window to build ancillary revenue capability before the cycle turns. That window is open now, while backlogs are still healthy and you have the cash flow to invest. It will close when backlog declines force you to cut overhead instead of building new capability.

The services Turner built did not appear overnight. SourceBlue launched in 2001. The Accelerated Payment Program started in 2014. Self-Perform Operations has been scaling for years. xPL Offsite formalized in May 2025 after two decades of prefabrication experience. First Equipment Company launched in January 2026 after piloting on large projects. This is a 20-year strategy that is now reaching critical mass at exactly the moment when the market is about to test it.

Every GC with ~$1 billion or more in revenue should be asking three questions right now.

What percentage of my EBITDA comes from services other than the CM fee?

If I had to bid at 1% fee to win a major project, would I still be profitable?

And if the answer to that second question is no: what am I going to do about it before Turner bids 0% on my best client’s next project?

Turner doesn't publish segment economics, so I built a model using industry benchmarks for each service category to model this out.

Fantastic write up!