The Captive Arbitrage

The carrier doesn't know what your prequal team knows. That information gap is money on the table.

General contractors run one of the most thorough risk assessment processes in any industry. Before a subcontractor sets foot on a jobsite, the GC’s prequal team has collected financial statements, EMR scores, OSHA logs, bonding capacity, references, insurance certificates, sometimes even org charts and key personnel resumes.

That’s effectively an underwriting submission. The GC has already done the work that an insurance carrier would need to do to price the risk. But in the current structure, that data sits in a prequal database, or worse, a shared drive somewhere, completely disconnected from the insurance program that prices the exact same risk.

The carrier writing the CCIP has almost none of this information at the individual sub level. They’re typically pricing the insurance wrap based on the GC’s aggregate loss history, the project type, the geography, and maybe the total sub cost breakdown by trade. They’re not underwriting each sub’s risk profile the way the GC’s prequal team already has.

The GC is paying a premium on insurance coverage that reflects the carrier’s uncertainty. That uncertainty is something the GC already resolved internally with prequalification.

What’s a Captive?

A captive is a licensed insurance company owned by its parent. If the captive is domiciled in a jurisdiction that permits the relevant lines of business and is adequately capitalized, it can underwrite GL (general liability), workers comp, builder’s risk, and CCIP/OCIP wraps on its own projects. Many of the largest GCs already operate captives. Zurich, Chubb, The Hartford, and other major construction program carriers know that their most sophisticated clients are either running captives today or evaluating them.

To be clear, this only works when the GC has enough premium volume, strong loss history, and the operational discipline to manage claims.

Stand up the captive in a favorable domicile. Start with the lines where the GC has the most data advantage and the most premium volume, typically GL and workers comp through CCIP structures. Build the actuarial track record over two to three years. Then expand into additional lines as the captive’s surplus grows and the reinsurance market gets comfortable with the program, and you will need reinsurance.

The Data Advantage

A captive flips the information asymmetry. The GC’s prequal data becomes the underwriting engine. You know which mechanical sub has a 0.6 EMR and pristine financials versus which concrete sub is thinly capitalized with a rising DART and incident rate. You can price CCIP enrollment accordingly, or more importantly, you can make better decisions about risk retention levels. Keep more risk on the subs you’ve already vetted as strong. Buy reinsurance for the tail exposure or the trades where loss frequency is harder to predict.

Then layer in the real-time project data. During execution, the GC’s field teams generate daily logs, safety observations, schedule updates, and RFI volumes. All of these are leading indicators of a loss. Pair that with existing and historical data from past projects and now you have an early underwriting engine. A sub falling three weeks behind schedule burning through twice the number of RFIs might be in over their head technically and could require additional insurance products like trade insurance. PMs and PXs know this. Carriers don’t.

None of this data flows to an insurance carrier today. In a captive structure, it can feed directly into reserving and risk management decisions.

The GC running a CCIP through its own captive is now capable of building a unified risk view across the entire project. The CCIP covers the casualty exposure from the sub’s work. The prequal data and project execution data give you the leading indicators that an external carrier can’t access. A captive structure lets you price that correlation properly.

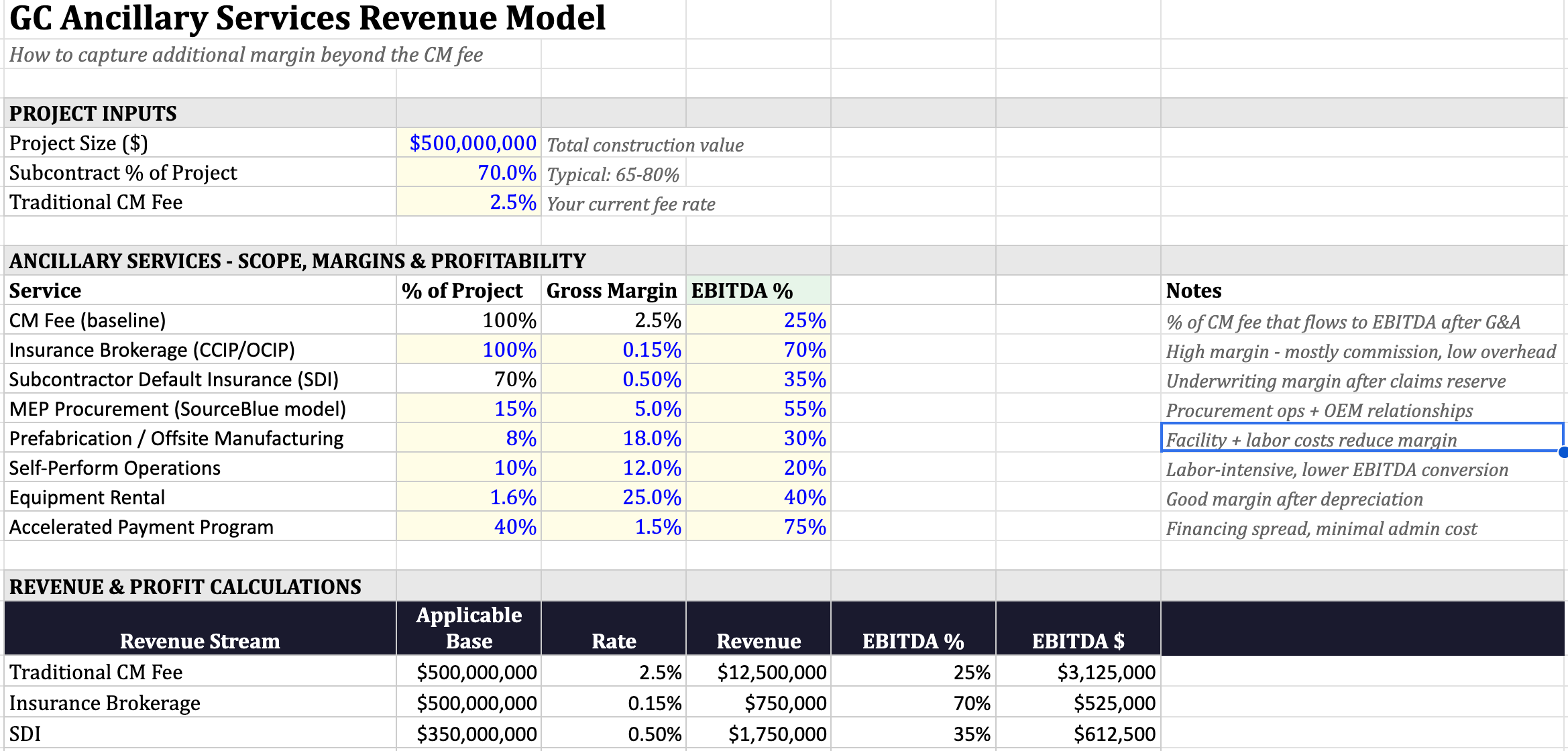

Right now in the model, insurance brokerage is positioned as a commission business. The captive argument is that a GC should be capturing the underwriting margin, not just the brokerage commission. The SDI line already assumes the GC is retaining subcontractor default risk at a 35% underwriting margin after claims reserves. That's the captive in action. The CCIP insurance and SDI lines together add $2.5M in revenue at blended EBITDA margins north of 45%. That's an incremental $1.1M in EBITDA from risk the GC is already managing operationally.

Every one of these ancillary lines exists because the GC sits at the center of the project's information and cash flows.

Why You Can’t Also Be a Broker

You can’t be a broker and run a captive without introducing serious conflicts.

A broker’s value proposition is built on independence. They shop the market on behalf of the insured, comparing coverage and pricing across carriers. The moment a broker also operates as an MGA or MGU, they’ve introduced a conflict.

The same logic applies to brokers who manage GC captives. If a broker is advising a GC on their insurance program and also administering that GC’s captive, they’re earning fees on both sides. They’re consulting on risk retention levels (how much goes into the captive vs. the commercial market) while simultaneously earning administration fees from the captive entity. Every dollar that stays in the captive is a dollar the broker didn’t place in the open market, but it’s also a dollar generating captive management fees. The incentives don’t cleanly align in either direction, which is almost worse than a clear conflict because it makes the bias harder to identify.

For a GC evaluating a captive, this means the decision about how much risk to retain is a capital allocation decision, not an insurance decision. It depends on the GC’s balance sheet strength, cash flow predictability, project mix, geographic concentration, and tolerance for volatility. A broker who also runs the captive has a hard time giving disinterested advice on those capital allocation tradeoffs.

Group Captives

The single-entity captive is the obvious move for a top GC with >=$1B+ in annual revenue. But the more interesting structural play is the group captive, where multiple GCs pool risk into a shared vehicle.

A single GC running $30M in annual construction insurance premium through a captive has a concentrated book. One bad project year, a crane collapse or a multi-fatality incident, can blow through reserves and force a capital call from the parent. A group captive with four or five large GCs writing $120-150M in combined premium creates diversification. Different project types, different geographies, different trade mixes. The reinsurance market prices that pool differently than it prices any individual GC’s book, and the rates reflect it.

The harder question is competitive dynamics. GCs compete for the same projects, often with the same subcontractors. Sharing prequal data through a group captive means your rival can see which subs you’ve vetted, how you’ve scored them, and implicitly, which ones you trust enough to carry risk on.

But look at what the credit card networks figured out decades ago. Visa and Mastercard are owned by banks that compete fiercely for customers. Those same banks share fraud data, transaction risk scores, and default information through the network because the shared infrastructure makes everyone’s individual book more profitable. The competitive advantage moved up the stack, from “who has better data” to “who uses the shared data more effectively in their own operations.”

The same logic applies here. If four top-50 GCs standardize their prequal frameworks and pool subcontractor performance data into a group captive, the result is something that doesn’t exist anywhere in construction today: an industry-level credit bureau for trade partners. Every GC in the pool benefits from a normalized view of subcontractor financial health, safety performance, and operational capacity. The competitive differentiation shifts from “who has decent prequal data” (everyone does) to “who acts on it best in pricing, project staffing, and risk retention decisions.”

Administration is the practical bottleneck for this type of product. Someone has to run the captive, and it can’t be any of the participating GCs without reintroducing the conflicts described above. A third-party captive manager with no brokerage or placement business is the clean structure. The captive board would include risk officers from each participating GC, with actuarial and claims functions outsourced to specialists. Group captives exist in healthcare, transportation, and energy. Construction is just late to the model.

The trigger that makes this happen is a hard insurance market when commercial carriers tighten capacity and raise rates on construction programs (which happens cyclically and is happening now in certain casualty lines). This also happens when the economic case for retained risk through a group captive becomes impossible for CFOs to ignore. The GCs that have already built the data infrastructure and prequal standardization should be able to stand up a group captive in 12-18 months for GL, workers comp, and SDI.

Compounding Advantages

Two to three years of loss data underwritten with superior information creates a performance history that reinsurers will price favorably.

This new entity owns the actuarial track record. Two to three years of loss data underwritten with superior information creates a performance history that reinsurers will price favorably. That pricing advantage compounds. Every year the captive operates with better-than-market loss ratios, the reinsurance terms improve, which widens the cost gap between the captive GC and competitors still buying coverage at market rates.

It owns the data asset. Structured prequal data linked to actual project outcomes (safety incidents, schedule performance, claims history) is the training set for underwriting models that get better over time. GCs building this have a two to three year head start that no amount of capital can compress.

And it changes the talent equation. The best project executives and risk managers will want to work at the GC where their operational discipline directly improves the company’s financial performance through the captive. A safety director whose programs reduce captive losses is visibly contributing to the bottom line in a way that’s impossible when insurance is just a line item managed by an external broker.

Don’t wait to watch insurance costs rise with the market while your competitors’ costs decline with their own performance. In a 2-3% margin business, that spread is the difference between winning work and subsidizing someone else’s risk pool.